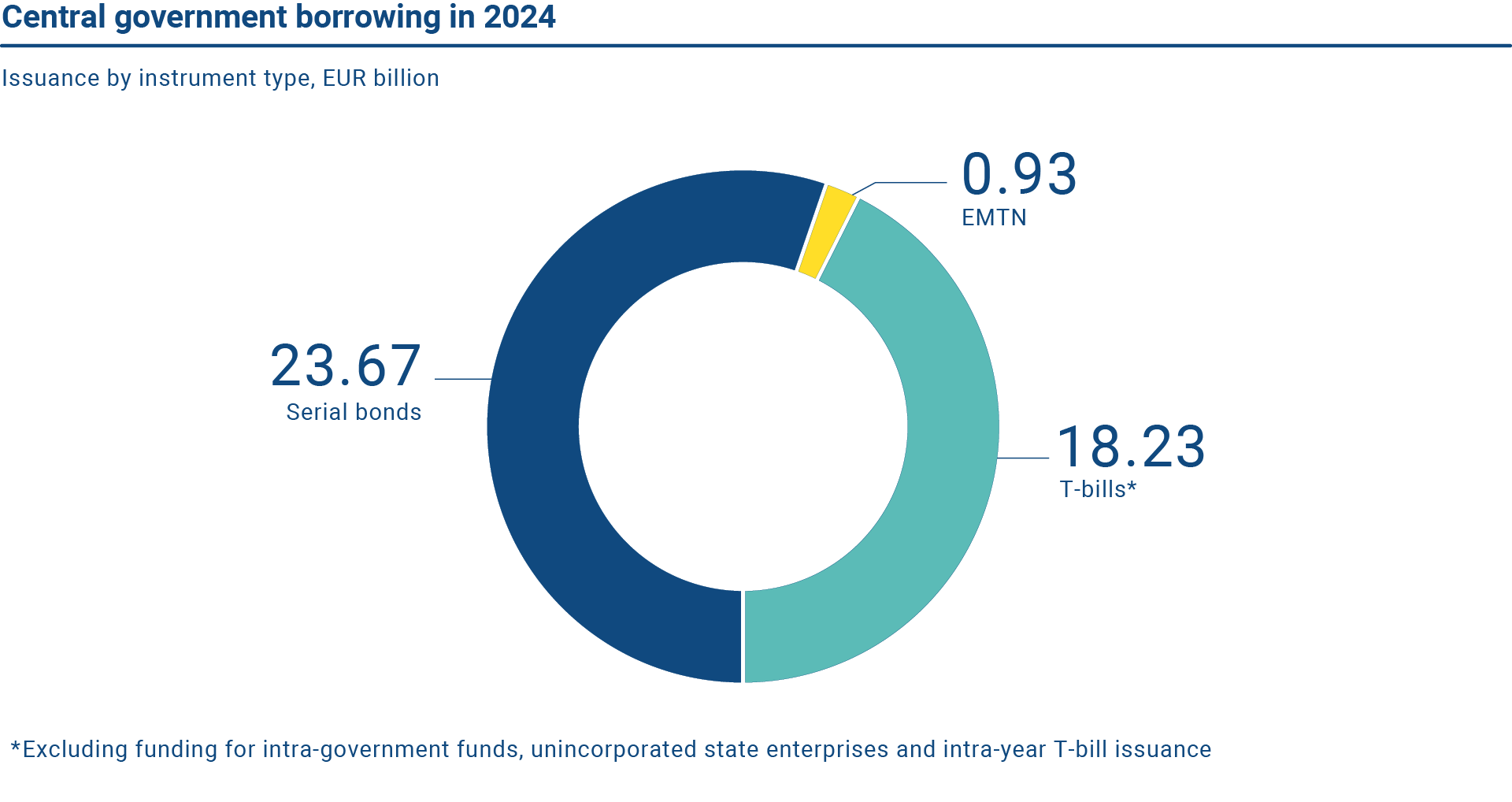

In 2024, the Republic of Finland’s realised gross borrowing totaled EUR 42.8 billion. Of this amount, long-term issuance accounted for EUR 24.6 billion (57%). The rest, EUR 18.2 billion (43%), was short-term borrowing. Realised net borrowing amounted to EUR 12.58 billion.

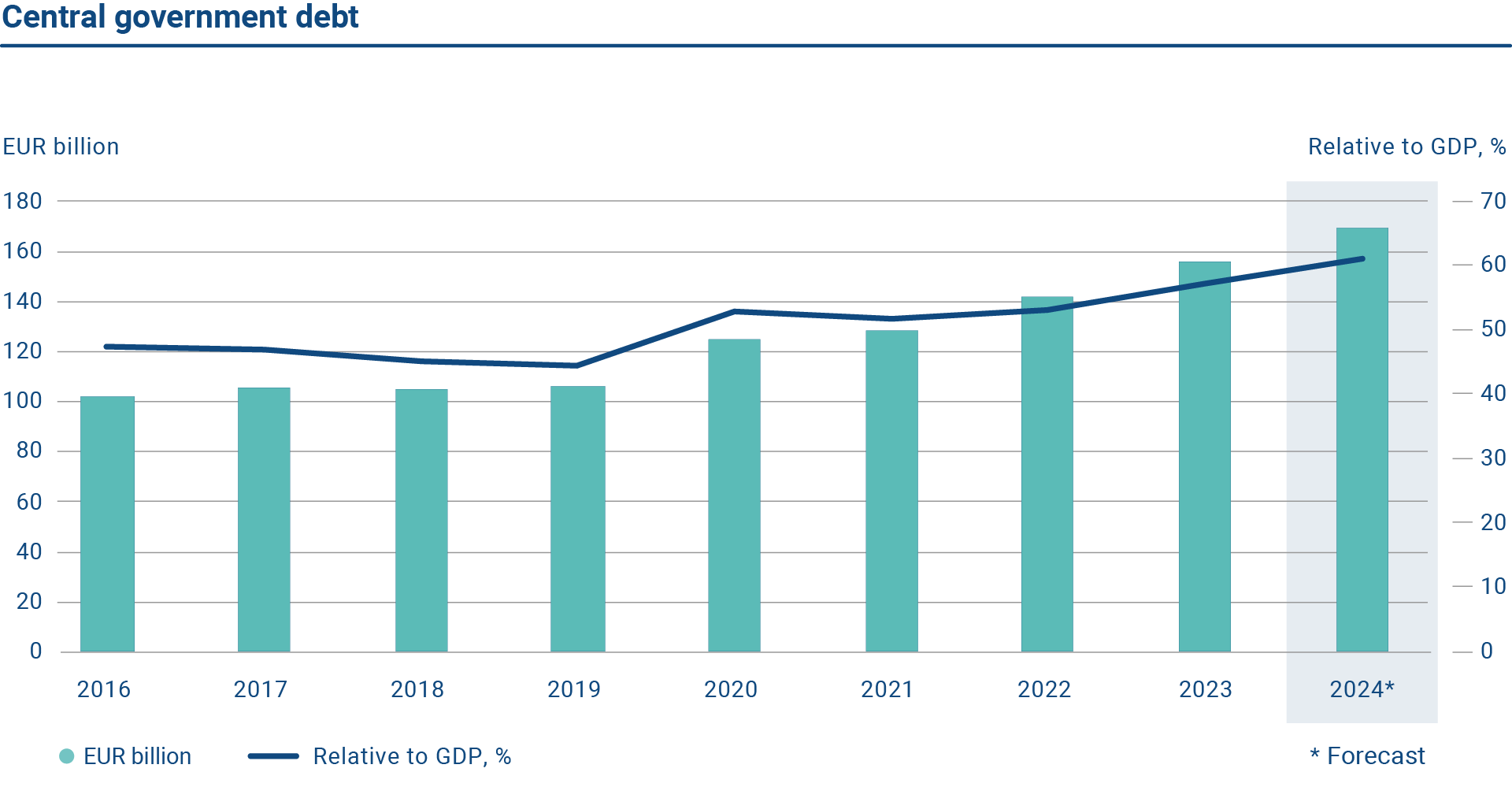

The central government’s gross borrowing requirement remains around EUR 42 billion in 2025, after which it is estimated to decrease to EUR 35–39 billion annually. At the end of the year, the central government debt stock reached approximately EUR 169 billion.

The realised gross borrowing amount in 2024 was EUR 42.83 billion. Of this amount, long-term issuance accounted for EUR 24.60 billion and short-term borrowing for EUR 18.23 billion.

The graph shows the volume of Finland’s central government debt and debt in relation to GDP in 2016-2024. The central government debt was EUR 169.41 billion at the end of 2024. The debt-to-GDP ratio was 61,20%.

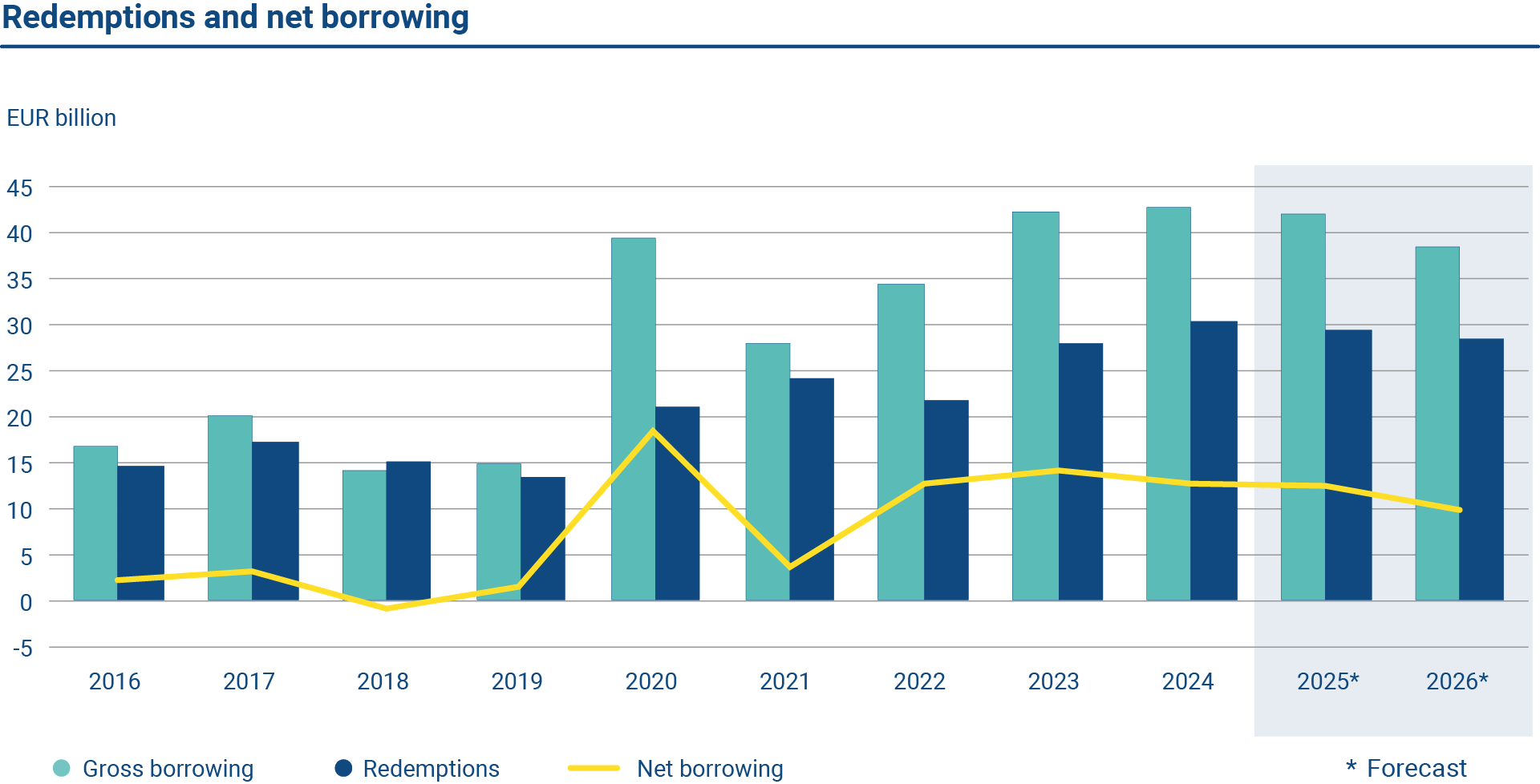

The graph shows annual gross borrowing, redemptions and net borrowing in 2016-2026. Redemptions of EUR 30.25 billion took place in 2024 while net borrowing amounted to EUR 12.58 billion.

According to the forecast by the Ministry of Finance, the estimated net borrowing requirement for the year 2025 is EUR 12.50 billion. With EUR 29.46 billion of redemptions, the gross borrowing requirement totals EUR 41.96 billion.

Funding strategy

The funding strategy of the Republic of Finland is based on euro benchmark bond issuance. New benchmark bonds are issued in syndicated form. Syndications are complemented with regular bond tap auctions, which raise the outstanding volumes of the existing bond lines. There is also a Euro medium-term note (EMTN) programme under which the Republic of Finland can issue bonds in foreign currencies to serve a broader investor base. However, issuance in foreign currencies is subject to market conditions, and a reasonable funding cost in comparison to euro issuance.

The current funding volume supports three new euro benchmark bond syndications per year, tap auctions of existing benchmark bonds and one benchmark-sized USD bond issue. The short-term funding is carried out by issuing Treasury bills. In terms of bond maturities, the annual issuance pattern of a new 10-year bond is complemented with a new long-term bond – either 15, 20 or 30 years – to maintain a liquid benchmark bond curve up to 30 years. This year, subject to market conditions, the State Treasury plans to issue a new 20-year benchmark bond. Due to the redemption profile, the third new benchmark bond in 2025 is likely to carry either a 7-year or 15-year tenor. Market conditions permitting, issuance in non-euro currencies, most likely a USD benchmark bond, may complement the long-term funding. The share of short-term funding, i.e. Treasury bills, is estimated to account for approximately 45% of the gross annual borrowing in 2025.

The objective of the State Treasury is to maintain Finland’s position as a recognised and reliable issuer in the markets and thus ensure the demand for Finnish government bonds in the future.

Funding operations and investor demand

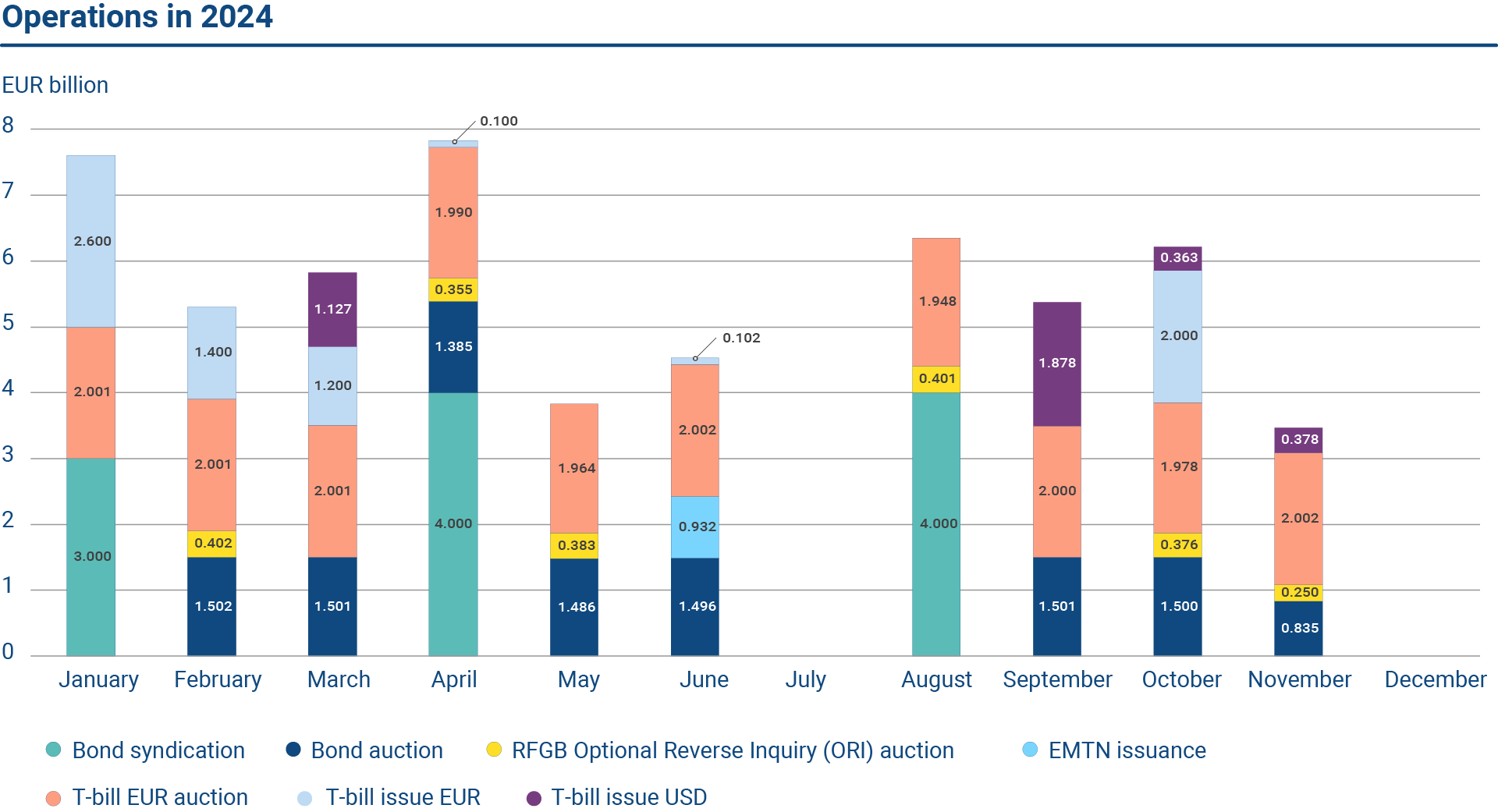

In 2024, the Republic of Finland issued three new euro-denominated benchmark bonds and one USD-denominated bond. A total of 14 benchmark bond auctions were conducted during the year. Short-term funding was carried out by issuing Treasury bills in auctions and in ECP format.

The graph shows the operations conducted by the State Treasury in 2024. Finland issued three new euro-denominated benchmark bonds, one USD-denominated bond, and arranged eight bond auctions. The short-term funding was carried out by issuing Treasury bills.

The first syndicated bond issue of the year took place in January when Finland raised EUR 3 billion with a new long 30-year benchmark bond. The bond has a maturity date of 15.4.2055 and pays an annual coupon of 2.95%. As customary, the top five performing Primary Dealer banks of the previous year were appointed as lead managers for the issue, and the other Primary Dealers as co-leads. The order book exceeded EUR 9 billion with over 90 investors participating in the transaction. The new 30-year line is the longest bond in the RFGB yield curve to date and attracted strong pension fund and asset manager participation.

The second syndicated transaction in April was a new 10-year benchmark bond with a maturity date of 15.9.2034. The bond was priced at 20 basis points over the euro swap curve to yield 3.016%. The bond attracted an order book many times greater than the issue size – EUR 23 billion – and included offers from over 160 investors. The broad-based demand allowed upsizing the deal from the targeted EUR 3 billion to EUR 4 billion at issuance.

The third euro-denominated syndicated issuance of the year was a new 5-year benchmark due 15 April 2030. The bond was issued in the latter part of August and was priced at 10 basis points over the euro swap curve to yield 2.550%. The high-quality order book of over EUR 10 billion and offers from more than 80 investors again allowed upsizing the deal to EUR 4 billion at issuance.

In June, the Republic of Finland syndicated its first US dollar bond in four years by raising USD 1 billion with a new 10-year bond that matures on 2 July 2034. The yield at issuance was 4.399%, which was 55 basis points above the mid-swap rate (USD SOFR) and 15.7 basis points over the pricing reference of UST 4.375% due 15 May 2034. Issuing in US dollars complements Finland’s euro-denominated borrowing and its purpose is to serve a more global investor base.

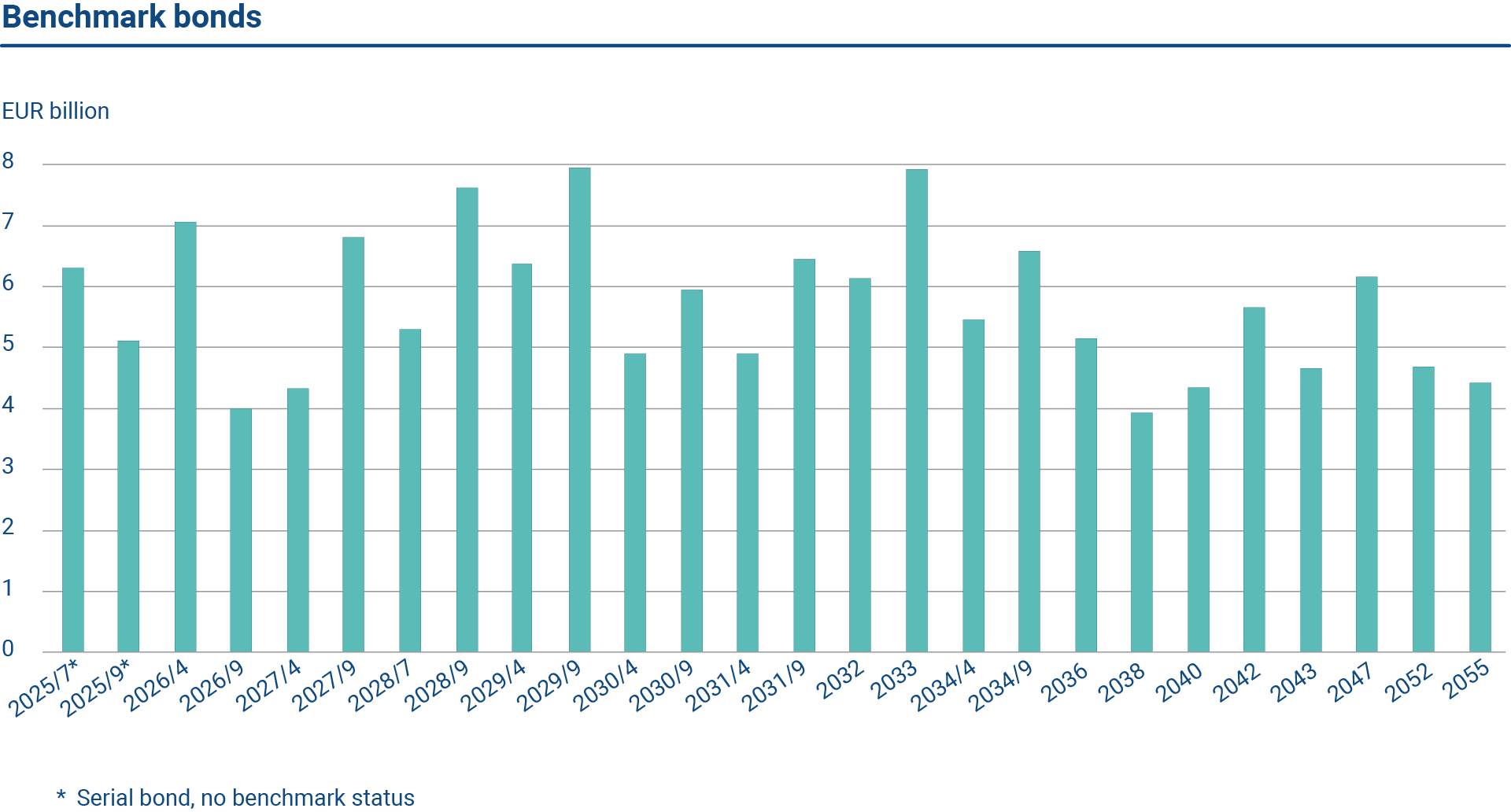

The graph shows all outstanding serial bonds issued by the State Treasury. Of these, the majority are benchmark bonds.

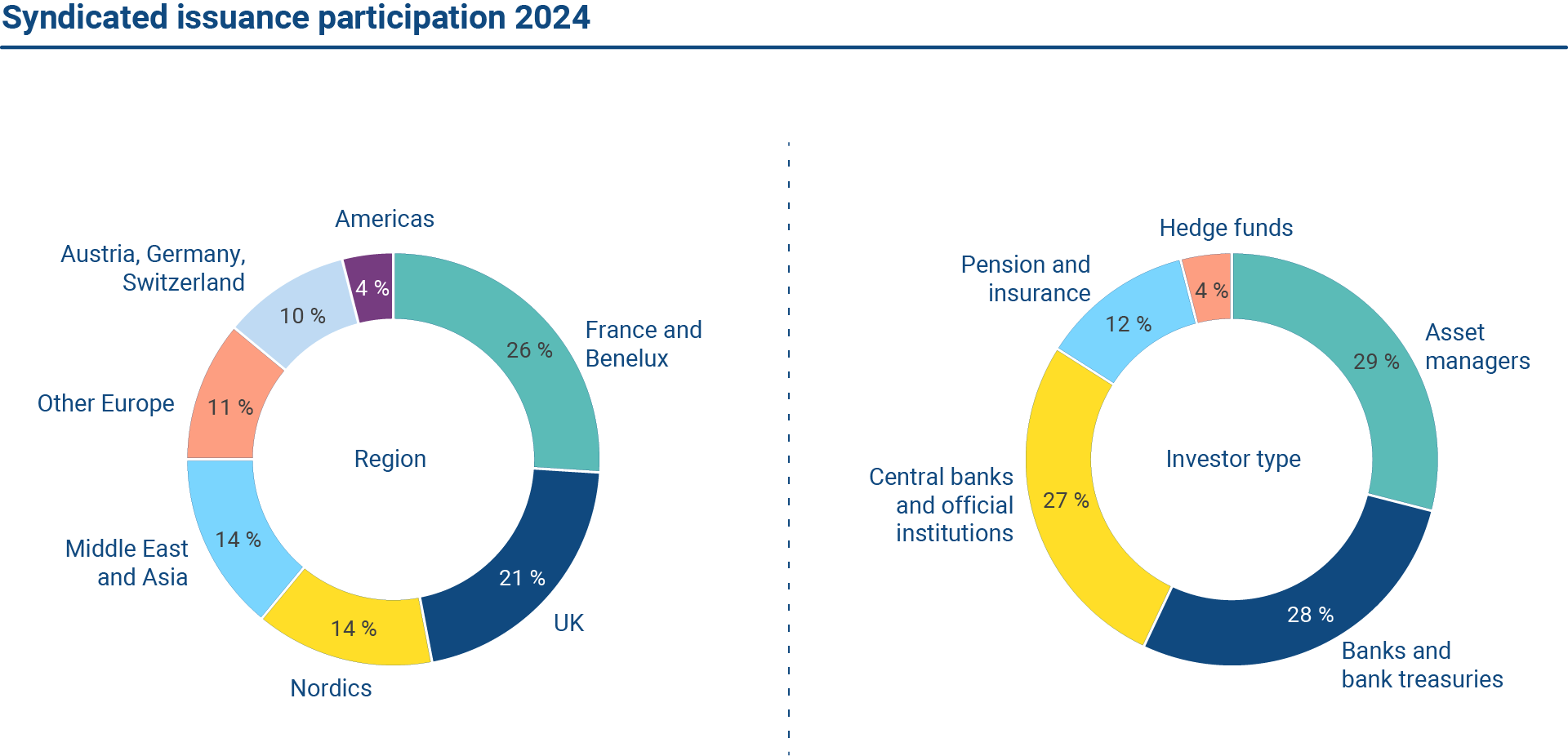

The graph shows the syndicated issuance participation in 2024 by region and investor type.

Tap auctions

In addition to the syndicated issues, the State Treasury conducts tap auctions on existing benchmark bonds in the primary market. An auction calendar is published quarterly on the State Treasury website. In 2024, eight regular benchmark bond auctions and six optional reverse inquiry (ORI) auctions were conducted in total. Five regular auctions were held in the first half of the year, and three in the latter part of the year.

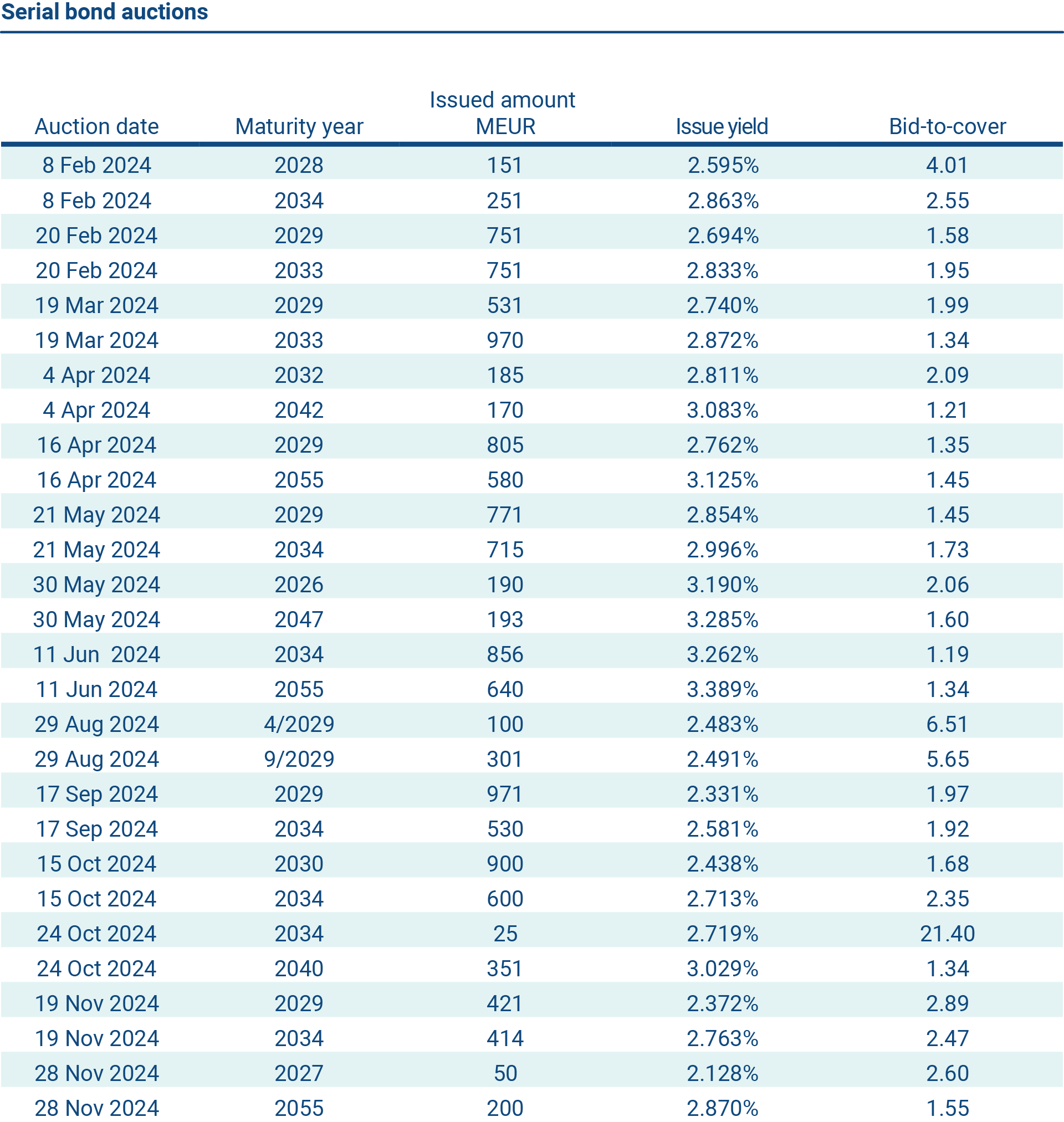

The total auctioned funding volume via benchmark bond auctions was EUR 13,373 million, of which EUR 2,167 million were from ORI auctions. All auctions were dual line auctions including two bonds with different maturities auctioned in the same auction. The bid-to-cover ratios for the auctioned securities (excluding ORI auctions) varied from 1.19 to 2.47. The issued amounts were between EUR 414 and EUR 971 million per bond per auction, excluding ORI auctions.

The table shows serial bond auctions.

Optional Reverse Inquiry Auctions

The State Treasury introduced ORI auctions for benchmark bonds in March 2023 and – following a positive response from the Primary Dealers – continued them in 2024. The purpose of the facility is to support the RFGB secondary market liquidity, by providing an opportunity for market makers to source off-the-run bonds in the primary market regularly.

An ORI auction is conducted only when one or more Primary Dealers express interest for a particular bond or bonds prior to a scheduled auction date. The number of potential auctioned lines is limited to two, and the maximum total amount to be issued is EUR 400 million.

Short-term funding

The State Treasury issues Treasury bills in euros and US dollars through banks included in the Treasury Bill Dealer Group, according to the financing needs of the central government.

Euro-denominated Republic of Finland Treasury bills (RFTBs) are issued via auctions. In auctions, the counterparties in the Treasury Bill Dealer Group can submit bids, and the price of the auctioned security is determined based on the received bids.

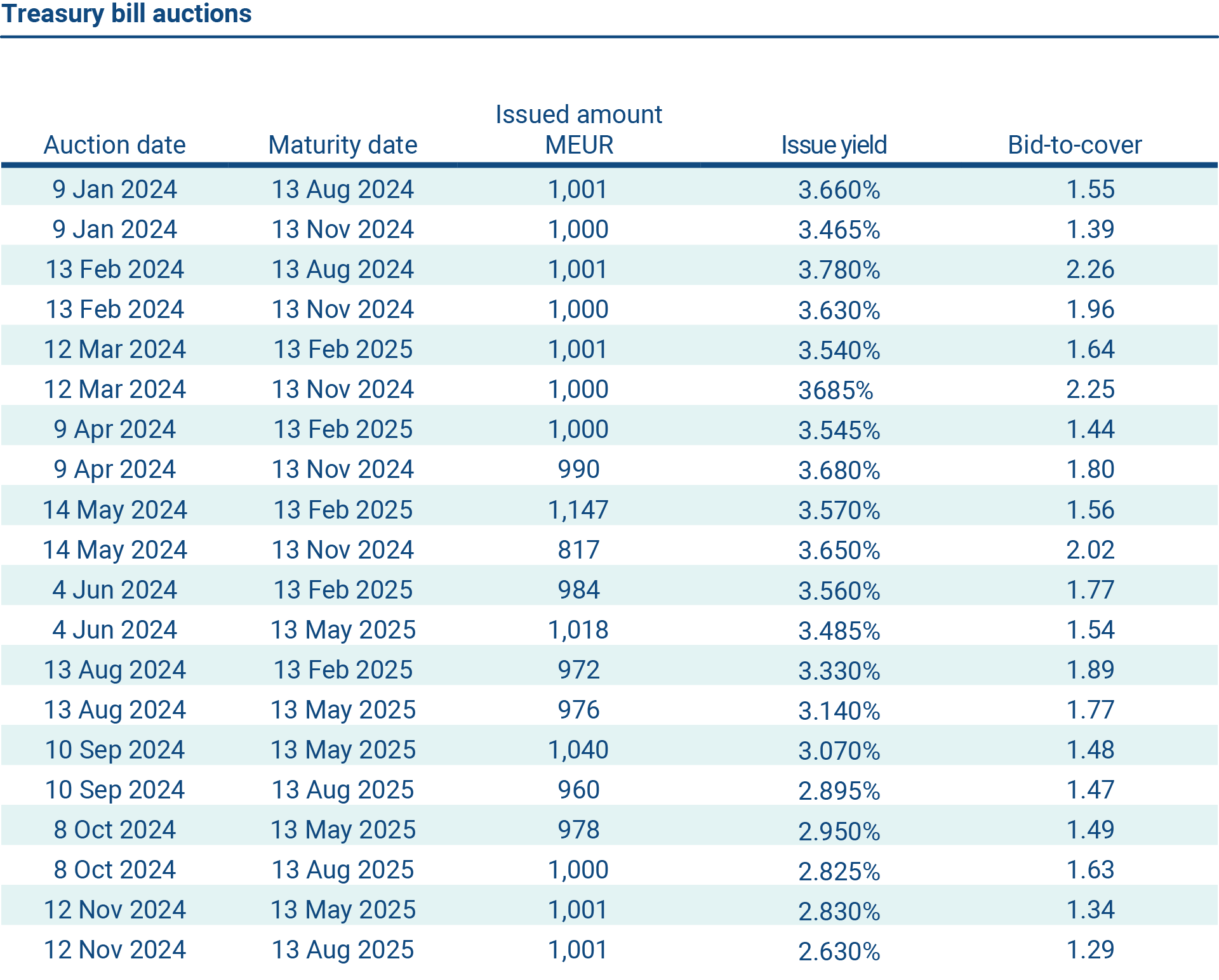

In 2024, the State Treasury held 10 Treasury bill auctions, raising a total of EUR 19,887 million, including funding for intra-government funds.

The table shows Treasury bill auctions.

The State Treasury may also issue Treasury bills on other occasions, depending on the demand and financing needs, in which case the State Treasury defines the reference price for the issue. This issuance method resembles that of Euro Commercial Paper programmes (ECP). Treasury bills in ECP format can be issued in two currencies: in euros and in US dollars.

In 2024, ECP format Treasury bill issuance was conducted both in USD and EUR based on pricing and demand during the year. The gross ECP issuance in USD was 4.1 billion and in EUR 7.4 billion.

The average maturity in USD ECP issuance was 7.8 months and EUR ECP issuance 8.0 months. The outstanding stocks of USD- and EUR-denominated Treasury bills at year end were USD 4,120 million and EUR 15,380 million (USD 1,800 million and EUR 19,062 million in 2023).

Liquidity management

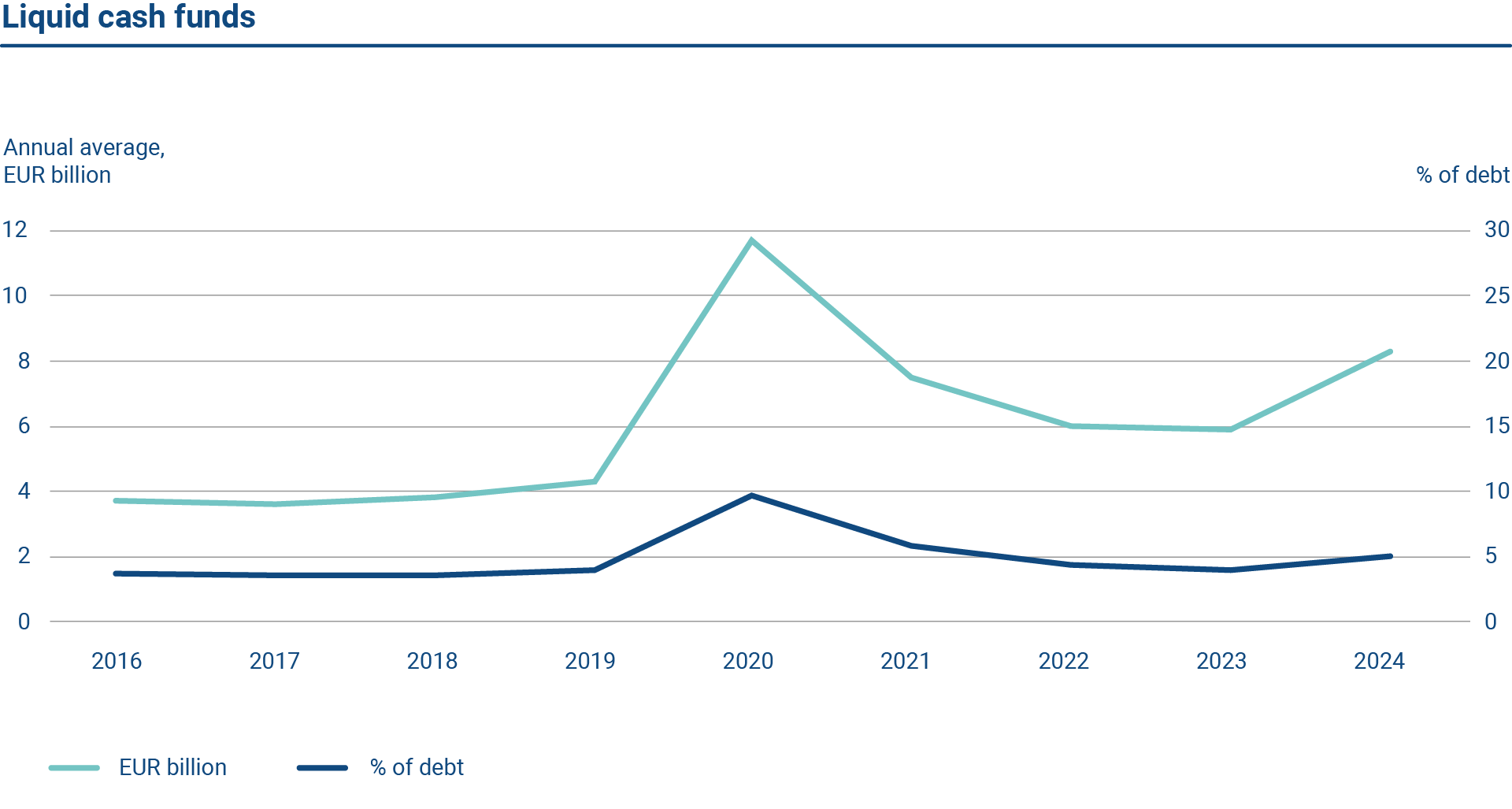

The amount of central government cash reserves varies daily depending on income and expenditure flows. The size of the cash buffer is based on an assessment of sufficient liquidity and a limit on uncovered net cash flows. The average size of central government’s liquid cash funds increased in 2024. This was due to changes in the debt management guidelines, set by the Ministry of Finance, where the central government’s liquidity limits were tightened. More information on Finland’s debt management strategy update can be found in Chapter 7.

Cash flows follow both intra-month and annual seasonal patterns due to timing mismatches in income and expenditure. Changes in the budget deficit during the fiscal year also affect liquidity management via changes in funding requirements.

As the primary focus is sufficient liquidity, actual borrowing may deviate from that budgeted for the fiscal year for various reasons, e.g., deferrable allowances which are budgeted in a specific year but used over a number of years. In 2024, central government’s realised borrowing exceeded the budgeted amount by approximately EUR 600 million as cash reserves were boosted before year end to secure sufficient liquidity. The requirement to post Credit Support cash collateral fell during the year, which reduced the funding need.

The annual average of liquid cash funds was EUR 8.3 billion or 5.0% of debt in 2024.

The cash reserves are invested in very short-term maturities using primarily bank and central bank deposits and triparty repos. The latter means depositing funds with eligible counterparties while receiving a bond or bill as collateral for the term of the deposit. The collateral is managed by a third party, e.g., central securities depository.

Liquidity management relies on the central government cash flow forecast system. All government accounting entities forecast their income and expenditure for the next 12-month period into the system. The State Treasury uses this data as a basis for liquidity management decisions.